If you have a vision for starting your own independent grocery, niche food store or quality produce shop, there can be several questions to consider. Your choice on the structure and nature of the legal business entity will have an impact on your tax and liability exposure. Starting a business requires a lot of research and some familiarity with business laws and regulations at a local, state, and federal level.

There are no good nor bad corporate structures or entity formats. Each has its own advantages and disadvantages. Here we provide an overview of the options available to help you gain a background understanding of your choices. We can’t give you legal advice – it’s best to speak to a lawyer for that. However, we can help you understand some of the concepts and questions you might want to consider.

What is a business entity?

William Perez, from The Balance, best described what a business entity is, “a business entity is an organization created by one or more natural persons [people] to carry on a trade or business. Business entities are created or formed at the state level, often by filing documents with a state agency such as the Secretary of State.”

Types of legal entities

Business legal entities come in various kinds: sole proprietorships, partnerships, limited liability company, and S and C Corporations. The IRS and the Earl Lowe Foundation put out a basic layout on what kind of entities are available for business owners and the pros and cons for each one.

Sole Proprietorships

A sole proprietorship means the business will have a single owner. That owner is responsible for 100% of the business and liable for lawsuits filed against the business. Since the owner is 100% responsible they also report the profits and losses of the business on their personal tax return. There are no state filings needed to create a sole proprietorship. It’s easy to start and operate and many small business owners tend to gravitate to this option.

Advantages of sole proprietorship

- All of the profits made in the business are yours. Since you’re the only owner you keep all the good (profits, success, growth) of the business to use at your discretion (of course keeping in mind tax and other regulatory requirements).

- It is also one of the simpler entities to set up, with a relatively small amount of paperwork.

- This form offers maximum authority within management and you get to make all the decisions.

Disadvantages of sole proprietorship

- Even though you keep all of the “good”, you are also faced with unlimited liability where you are also responsible for all the “bad” – e.g. law suits.

- Under a sole proprietorship, your own personal money (not necessarily derived from the business) is liable for settling lawsuits, taxes, penalties, etc. If you are faced with legal disputes – you are personally liable (rather than the business being recognized as a separate legal “person”.)

- The limited ability of to raise capital is a disadvantage many business owners face. Sole proprietorships are not structured to take advantage of certain tax benefits that a corporation might receive for offering disability insurance, medical insurance, and life insurance.

General Partnerships

According to the Uniform Partnership Act, a general partnership is an “association of two or more persons to carry on as co-owners of a business for profit.”

Many people choose to add a partner into their business because they share the same passion of being a business owner in whatever industry they have chosen and would like to share the burden, pressures, responsibilities and also the wins of owning and running the business.

People often choose partners based on the skills and/or expertise they have. People sometimes compare a general partnership to a marriage since you have to put in a lot of effort and trust in sharing your business with someone!

Advantages of general partnerships

- Easy to start up and minimal paperwork. (Do not have to register with the state)

- Responsibilities are usually shared between partners for example, financial pressures, decision making and many more.

- Partners are required to file a federal tax form called Form 1065 but, usually no income tax is paid. The partners are required to file the business income or losses on their individual income tax returns.

Disadvantages of general partnerships

- Generals partners all have unlimited liability for the business. This means every decision made without proper precautions could harm the partners. This also includes debt and taxes. Partners can be joint or severally liable – meaning that if your partner does something wrong, your personal finances can be legally at risk.

- Since responsibilities are shared one partner’s decision might not sit well with another – this may cause conflict or damage the business.

- A business would be terminated in a partnership agreement if a partner passes away or withdrawals from the agreement.

Limited Partnerships (LP)

Within a limited partnership, there tends to be division in responsibilities shared for partners. There are limited partners who are considered “silent partners” since they really can make any of the decisions or control over the day-to-day operations. Limited partners are usually there to make investments in the company and act as a source of capital. The types of companies that tend to gravitate to this type of partnership are usually law firms, accounting firms, finance firms, and real estate companies.

Advantages of Limited Partnerships

- There are many advantages to being part of an LP. If you’re the general partner of the LP you have complete control of the management of the company.

- For the limited partner, there are advantages as well since they’re on liable and responsible for only the amount they invested and nothing more.

- A limited partnership’s income is not taxed at the business level; instead, business profit and loss are “passed through” to the partners for reporting on their personal tax returns.

- More limited partners could be added to increase business capital (to buy in as a partner).

Disadvantages of Limited Partnerships

- Something a general partner needs to take into consideration is that within a limited partnership they would hold unlimited liability for the company and the actions of other general partners.

- Many states require extensive paperwork when creating a limited partnership. This is done to establish the responsibilities of general partners and limited partners to avoid disputes and define protection to the limited partners.

- Since limited partnerships can be complex usually professional legal assistance is required and that leads to hefty fees from those individuals.

Limited Liability Company

LLC or in other words a Limited Liability Company is a business structure allowed at the state level. Many states don’t have restrictions on ownership, this allows individuals, corporations and other LLC’s to be considered members. Jane Haskins Esq., from LegalZoom listed a few advantages of a LLC. On the other hand, Rod Howell, from the Small Business Chron, listed a few disadvantages a LLC have that might affect your small business.

Advantages of Limited Liability Companies

- LLC’s share the same tax treatment as a partnership, sole proprietorship, C Corporation, or a S Corporation. This entity can use “pass-through” taxation where you can avoid paying corporate taxes and will only be taxed on profits made by each owner.

- Flexibility within an LLC is a very attractive trait to many potential business owners. For example, there is no limit to how many owners there could be or what type. Also, there is no fixed management structure and owners decide the way they make decisions or how business is conducted.

- LLC’s have the advantage where there is limited liability for all parties involved. Meaning personal property and accountability can be separated and protected from that of the business.

Disadvantages of Limited Liability Companies

- Even though one of the advantages is that there is a limited liability there are still exceptions where this is not the case. For example, members of the LLC would be responsible for the actions of the company if they use the company to commit fraud, personally guarantee to repay a debt or negligently supervise the actions of an employee or another member that causes harm to a third party.

- The LLC is also one of the more expensive entities to setup and maintain. LLC’s are required to pay annual fees and make periodic filings with the state they’re affiliated with. LLC’s can receive different treatments within different states and certain businesses are ineligible to operate under an LLC for example, a bank or insurance company.

- Even though an LLC can use “pass-through” taxation to avoid corporate taxes they must have at least two members to qualify. If not, the company would have to file taxes as a sole proprietorship or corporation. The LLC can lose the privilege of its “federal tax exemption” if 50% or more of its capital and profits interest are sold or exchanged within a one year period.

Corporation

Out of all business structures, the corporate entity is one of the most complex, and involves the most amount of paperwork. A corporation is organized on the state and federal level and the ownership is divided into shares of stock. A corporation can be classified in two ways, C Corporation,

Similarities of C Corporation & S Corporations

- Both C and S Corporation follow the same basic corporate structure. Both entities are required to follow corporate formalities. For example, issuing stock, electing board of directors, and holding meetings with stockholders and board of directors.

- Another similarity is that both entities offer limited liability and protection to shareholders when it comes to dealing with issues involving business debt.

- Both entities are required to file the same types of formation documents called the Articles of Incorporation or Certificate of Incorporation.

Differences of C Corporations & S Corporations

- The main difference when it comes to these entities is the way they’re taxed. The C Corporation is taxed as separate entities, file a corporate tax return (Form 1120) and pay taxes at the corporate level. On the other hand S Corporations are pass-through tax entities. They file the Form 1120S, similar to the 1120 but, in this case they don’t pay taxes on their income at the corporate level.

- S Corporations are limited to 100 shareholders in the company and they must all be US citizens/residents. On the other hand C Corporation’s are not limited to how many shareholders they have or if they’re US citizens/residents or not.

- To qualify for tax exemptions, S Corporation’s are not allowed to be owned by C Corporations, S Corporations, LLCs, partnerships and some trusts. With a C Corporation there is a freedom to be a shareholder not matter what entity you are.

Which Structure Should You Choose?

Hopefully with an overview of the basic pros, cons, risks and advantages of each legal entity, you are in a better position to narrow down or select a structure for your quality food store. For entrepreneurs with hopes of starting a natural, craft, or specialty food store, many recommend commencing with a sole proprietorship or a general partnership with someone qualified and who shares the same vision.

These two structures may work best for “beginners” and startup owners. They both require the least amount of paperwork and so may allow you to open your business in a shorter amount of time. However, it is best to consult with a lawyer as to your unique circumstances and about protecting yourself and assets from risk.

As time goes by and you see the business is doing well then, maybe you would consider bringing in a limited partner or you could also choose to incorporate as an LLC. From there if your business expands to multiple states and business is booming then you may consider changing to a corporation.

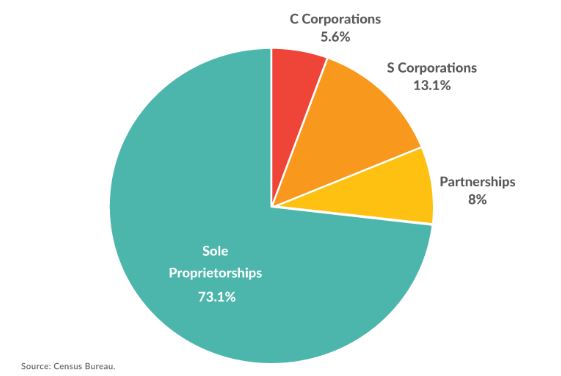

Below there is a chart from U.S. Census Bureau, that depicts the business entity market in 2015. This gives you a good sense of what kind of business structures are more popular and more common.

Choosing the way you decide to start your business will be an obstacle you will be forced to face. With the information given hopefully you make the best decision for yourself and for your business. As a business owner, you should always do what is best for business and follow the vision and goals you have set for your business.